Microfinance institutions (MFIs) provide small loans, small savings and small-scale financial products and services to people with economic vulnerability. Despite their key role in today’s economy, the industry can be difficult to operate in. Digitalisation efforts, such as establishing an ID assurance system, can help MFIs overcome many of the obstacles faced by the sector.

Microfinance vs Banks

MFIs provide financial services to the unbanked and underbanked communities that do not have access to traditional banks. These could be due to a multitude of reasons, such as:

- Slower processing times

- Unfulfilled requirements

- The need for collateral

- An established credit history

Microlending, which is a major part of microfinance, can be a lifeline for this consumer group. The influx of funds can be used to manage emergencies, acquire immediate household assets, capture rare business opportunities, or help a loved one. This emergency credit provides financial options to those going through these pivotal moments.

Although traditional banks do offer similar solutions, such as overdraft and fast-cash withdrawals via credit cards, the interest rates on these schemes can be dizzying. This assumes that the target consumers have access to these services in the first place.

More importantly, what makes microlending unique is the speed and accessibility in which the funds are distributed. While traditional loans take up to weeks for approval, microlending is intended to be quick to access. This is why many MFIs are localised and township-based.

Digitalisation is the way to go

These unique properties of microfinance makes the industry a prime target for digitalisation.

Digitalisation can help MFIs capture a larger customer pool compared to brick-and-mortar methods. Rather than visiting a local physical branch, MFIs can leverage mobile apps to capture the large number of mobile users in Malaysia. As of 2020, 90.1% of Malaysians have access to the internet, while 98.2% have access to a mobile phone.

Instead of accessing financial services during office hours, users can access microfinance services 24/7. In fact, users are now more comfortable making financial transactions through mobile phones thanks to the introduction of banking apps and e-wallets — thus lowering the barrier to entry.

Implementing these new IT systems require resources, but MFIs are also faster and more agile than large incumbent banks, making it easier to apply rapid changes and development. Adopting mobile and digital elements makes MFIs more competitive, as investments and market demand is shifting away from traditional approaches to FinTech.

Barriers to digitalisation

Lack of user trust is a major obstacle against digitalisation, especially for an industry that provides quick and easy access to funds.

Traditional email and password systems alone do not apply here. There is a risk in fraudsters creating fake accounts, just to abandon them when they receive funds from microloans. Experian & CyberSecurity Malaysia reported a 76.6% increase in personal records found in the dark web over the last 18 months since 2020, making it easier for cybercriminals to create such accounts.

Implementing an ID Assurance system within your pipeline is important in verifying a user before conducting any transaction.

Obtaining regulatory approval to operate an online money lending business is also another hurdle within the industry. In 2021, the Ministry of Housing and Local Government of Malaysia (KPKT) issued guidelines for online moneylenders. Here is the main gist of it:

- The MFI must be an existing licensed moneylender

- Must provide suitable IT infrastructure to host the online platform.

- Have independent parties to perform “security system assessment” on the dedicated servers

- Obtain approvals from both KPKT and police authorities.

Beyond the stated guidelines, there is also a need to collect the user’s proof of identity and implement digital e-signatures for funds to be distributed. These guidelines and systems are in place to protect the interest of both MFIs and direct consumers themselves.

Leverage AI Technology to Grow Your Microfinance Business

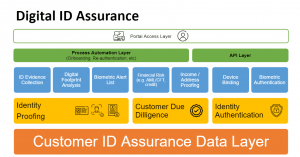

Innov8tif has the right tools to ensure that your customers are genuine and legitimate, serving as the foundation for any digitalisation efforts. We have developed the CIDA framework, which helps companies properly plan and scale their ID assurance systems.

Our solutions is broken down into three large verticals:

- Identity Proofing

EMAS eKYC is Innov8tif’s most demanded product. Consumers only need to capture a selfie and their ID Document to have their identities proven. AI algorithms run in the background to ensure that the user is who they say they are, and the photos captured are not spoofed, tampered or faked. Beyond eKYC, we also conduct digital footprint analysis, and biometric checks.

- Customer Due Diligence

Innov8tif can conduct automated background checks as well, to identify criminal history, credit score schecks, bankruptcy status and more. While MFIs have a higher risk tolerance than traditional banks, having more visibility over the customer profile is crucial in making loan distribution decisions.

- Identity Authentication

While identity proofing is mainly used during the registration process, identity authentication is applied for account access or regular transaction use. Biometric authentication services, such as facial recognition, can be used to authorise transactions. We can bind accounts to certain devices, restricting random accesses to accounts.

Through Innov8tif, MFIs can gain access to the same ID authentication services used by major banking institutions and telecommunication providers in Southeast Asia. We have presence in all ten members of the ASEAN region, implementing solutions in companies both large and small.

Digitalisation starts with having a clean customer database with high integrity — no bots, no cybercriminals, and no scammers. Although leveraging technology has been a trend even way before the pandemic, the integrity of your business’ customer database should not be the bottleneck.

Interested to learn more about us? Visit our homepage to learn more about our solutions, or get in touch at [email protected]!