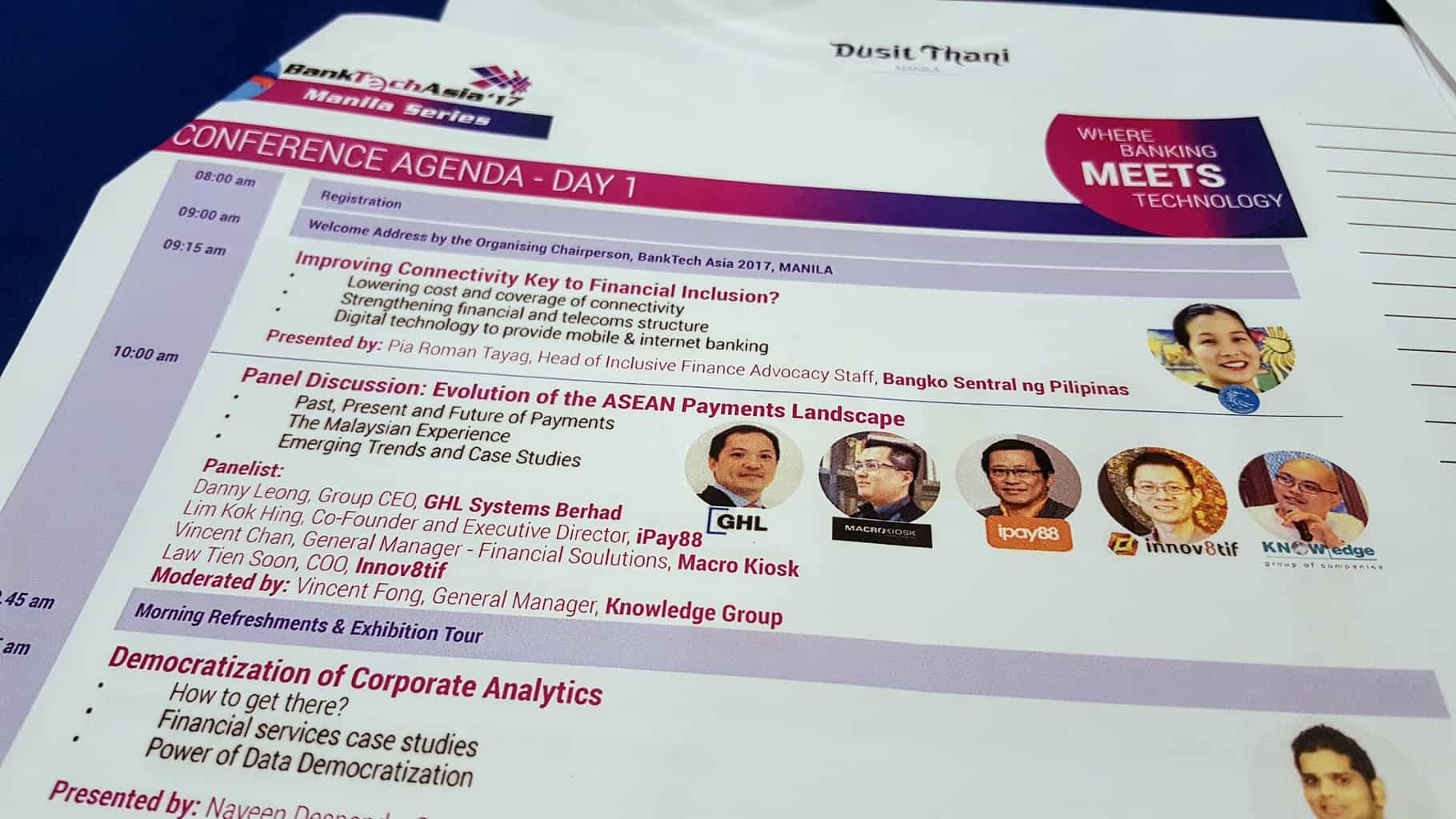

BankTech Asia is a series of annual events where banking meets technology. Last week, on 19th-20th Sep, BankTech Asia 2017 Manila Series was held in Philippines, and Innov8tif is honoured to be invited by MDEC as a speaker for panel discussion titled “Evolution of the ASEAN Payments Landscape“.

Mr. Tiensoon, our COO, represented Innov8tif for the panel discussion with other payment industry leaders – Mr. Danny Leong of GHL Systems, Mr. Lim of iPay88 and Mr. Vincent Chan of Macro Kiosk. This session was moderated by Mr. Vincent Fong from Knowledge Group.

Some of the key points discussed during this forum were:

- Past, present and future of payments

- Emerging trends and case studies

Crystal Ball?

While every panelist agreed that smarpthone had and is playing a vital role in the evolution of payment technologies and trends, but the emerging trends are evolving so quickly that, almost no one can assure what exactly the future big waves would be. There are technologies that “came and gone off”, quickly, due to lack of adoption, or untimely emergence. Nevertheless, artificial intelligence (AI) is a clear sign for what’s foreseeable, and the world is certainly going to be more cashless than ever. Mr. Tiensoon made the following remarks about what AI has to offer for payment industry.

Nowadays, I think nothing “new” you hear this year could escape from the word AI – artificial intelligence, which comprises keywords such as machine learning, deep neural network, robotic. Chatbot is a good example of AI-powered product that has reached a matured state in recent years.

In eKYC, as the onboarding processes have to be as automated as possible, ideally, AI will definitely play a key role. The mobile OCR (scanning with smartphone camera in layman description) of ID card that we have deployed to most of the telcos in Malaysia, is an example of computer vision technology. Another application of computer vision – is facial recognition, to automate the sighting process remotely without customer’s physical presence at branch. And, both ID card scanning and facial recognition technologies can get better, with machine learning. As the machine learns from more examples, it knows better at differentiating and recognizing the patterns and contents of a specific ID card.

In China, facial recognition is applied in every imaginable use case in fintech. You have cash withdrawal ATM that performs facial recognition as the 2nd factor of authentication; you have Alipay that uses facial recognition as part of eKYC process; and now you have KFC Hangzhou that welcomes payment with a smile!

Embracing Competition

In business, there shall be no permanent enemy. Or, in Chinese proverb – “one more friend is one less enemy”. Alipay has become so huge, so successful and widely adopted in China, that it is now going global. It is not hard to spot the “Alipay” sign in major international airports popular among Chinese tourists, especially in duty-free shops and tax refund counter. Two panelists in this forum – GHL and iPay88, are good examples of how their businesses are benefitting from Alipay’s global expansion into Southeast Asia. GHL has partnered Alipay to offer Malaysian in-store merchants and online merchants an alternative payment method, while iPay88 supports Alipay as an additional payment method through its gateway.

CIMB – one of the top 10 ASEAN bank brands, welcome Alipay by acting as the settlement and merchant acquirer bank to facilitate Alipay payments in Malaysia.

eKYC

The moderator also asked Tiensoon’s opinion about eKYC challenges in ASEAN: “We are seeing a lot of interests in cross-border remittance in the payment industry. Payment gateways and new fintech companies are jumping onto the remittance bandwagon. What are the eKYC challenges witnessed in ASEAN in general?“. And he shared Innov8tif’s view as follows:

For fintech companies and mobile wallets to flourish in the remittance pie at large scale, customers onboarding must ultimately be self-service. Self-service customer onboarding is an area that garners the highest interest within the banking and fintech area this year. Which also means, the KYC process must be evolved into eKYC (electronic KYC). And the new paradigm shift, is posting a new set of challenges not just to the banks and fintech companies, but ultimately the regulators – Central Bank in this context.

Using Malaysia as example. As the citizens are already equipped with national ID which has a chip containing thumbprint for verification purpose, the Central Bank requires that KYC is independently done by each bank or financial company providing money services. And as this method has been recognized for so many years, as the only reliable and trusted KYC method, it becomes a stumbling stone now in the digital customer self-onboarding age. The only way that a customer can complete the stringent KYC process, is to have his/her MyKad verified with fingerprint verification, which, requires presence of specialized hardware. And it is making it very challenging for any new fintech company to compete in the mobile wallet and remittance pie, when it comes to customer acquisition. Bank Negara Malaysia (Central Bank of Malaysia) is planning to regulate eKYC processes for remittance transactions, with the new standards to be finalised by October this year.

In Singapore, the government is already rolling out a new digital ID service known as MyInfo. And it is already in the piloting stage with UOB, DBS, OCBC, and Standard Chartered Bank. Customers with a voluntary enrolment into MyInfo database, will be able to sign up a new bank account, 100% online, without needing to submit any additional supporting document.

In Thailand, the Bank of Thailand is staying ahead in the eKYC game. A set of new regulations has already been released to facilitate eKYC. The guideline in Thailand requires “same standard” of face-to-face relationship in eKYC as the traditional KYC. And electronic method is permitted to conduct face-to-face interaction. Which means, a video call is all that’s required! Banks and fintech companies can expand market reach without investing into heavy capex as seen in traditional branch expansion model.

In Philippines, the proof-of-ID comprises too many types of possible documents. Fortunately, the House Committee on Population has recently approved the bill pushing for national ID system. It would be interesting to see, if Philippines would be the first country in ASEAN to have a nationwide national ID system that allows online validation.

Out of ASEAN, China and India are the 2 countries that already have the most eKYC-friendly national ID system in place. For this reason, the fintech sector is booming more rapidly than one would expect.

Payment industry has always been a key and interesting industry to watch in the financial sector. As it involves the flow of money, it is highly regulated by very stringent guidelines and regulations around the world. Yet, this is a fast-evolving and highly competitive industry that requires creative use and adoption of technologies, while at the same time staying within the compliance parameters and regulator’s radar.